Welcome to the Fall 2025 Pomona Newsletter

“Far more money has been lost by investors trying to anticipate corrections than has been lost in the corrections themselves.”

- Peter Lynch

Quick Takeaways:

- Global markets posted strong third-quarter gains, with U.S. stocks and bonds leading the way.

- Interest rates finally began to decline after the Fed’s first rate cut in over a year.

- US valuations remain stretched, with the Shiller CAPE ratio near historic highs.

- Despite attractive short-term yields, cash remains a poor long-term investment.

- Washington updated its estate tax rules for 2025—good news for small to mid-size estates, higher rates for larger ones.

- I attended two major industry events (Alternative Investment Forum and Future Proof Conference) to stay ahead of trends shaping the future of wealth management and investment opportunities.

As always, please let me know if you have any questions or would just like to chat. My cell is (509) 643-6028 or schedule a virtual/in-person meeting HERE if that is preferable.

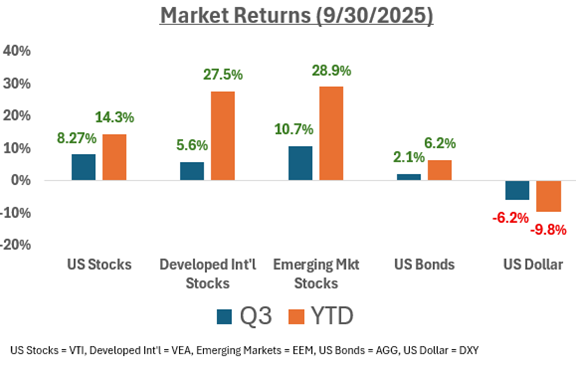

Markets Recap: Q3 2025

Bolstered by strong performance in September, both global stocks and bonds finished the third quarter solidly in the green. The S&P 500 hit another record high—its best September in 15 years—thanks to resilient consumer spending and continued strength in technology stocks. International stocks are up an impressive +27-29% for the year, benefiting from a weaker U.S. dollar (–6% for the quarter, –10% YTD). U.S. Treasuries rallied as yields declined following the Fed’s 25 bps rate cut on September 17.

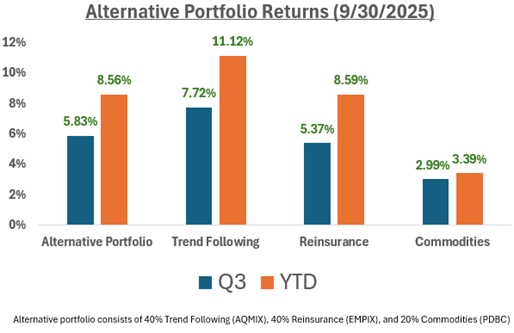

Alternative investments posted positive returns across the board, particularly within managed futures and reinsurance strategies. These strategies continue to play an important role as potential buffers in the event of a stock market decline.

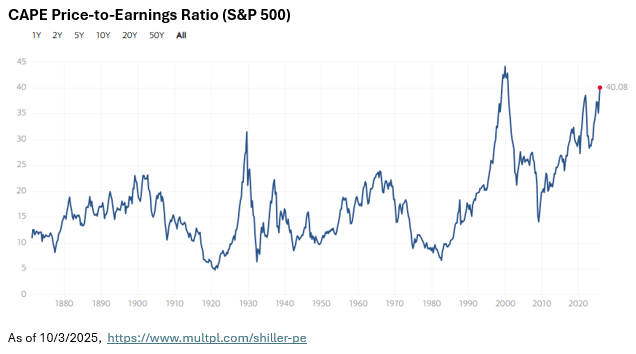

Valuations- High and Rising

Large U.S. stocks remain expensive by historical standards. As of early October, the Shiller CAPE ratio sits near 40, a level rarely seen outside of major market peaks. Historically, markets priced at similar levels have delivered below-average 5–10 year returns.

This doesn’t mean a market crash is imminent—but it does suggest that expectations should be tempered.

Our takeaway:

1) Keep return expectations realistic, don’t swing for the fences.

2) Diversify broadly—across regions, company sizes, and investment factors, not just large U.S. companies.

3) Maintain balance between stocks, bonds, and alternatives.

4) Actively rebalance your portfolio to stay aligned with long-term goals.

Interest Rates –Turning the Corner

After a prolonged tightening cycle, the Federal Reserve and Bank of England each cut rates by 0.25% this quarter, signaling a turn toward easing. Inflation remains sticky but improving: 2.9% headline and 3.1% core in the U.S. Bond yields have drifted lower, providing a tailwind for portfolios.

The consensus outlook for 2026 suggests one or two additional rate cuts as inflation normalizes and growth stabilizes.

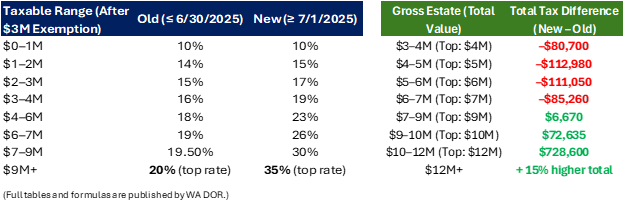

Washington State Estate Tax Update

Washington’s Estate Tax Update Amid Budget Shifts

After posting a $15 billion budget surplus in 2022, Washington State now faces projected deficits of roughly $4.35 billion for 2025–2027 and $6.7 billion for 2027–2029. Rising and expanded program costs - along side slowing revenue growth - are the main drivers. One step lawmakers took to help address this gap was updating the state’s estate tax, effective July 1, 2025.

The changes bring a mixed impact:

Higher exemption: The estate tax exclusion rises to $3.0 million, reducing or eliminating tax for many small and mid-sized estates.

Higher top rates: The brackets were adjusted, with the top rate increasing to 35%, meaning larger estates will face higher taxes.

In summary, under the new law, estates under roughly $6 million will generally owe less estate tax due to the higher $3 million exemption. Once an estate exceeds that range, the benefit of the exemption is offset by steeper marginal rates, leading to higher total taxes for larger estates.

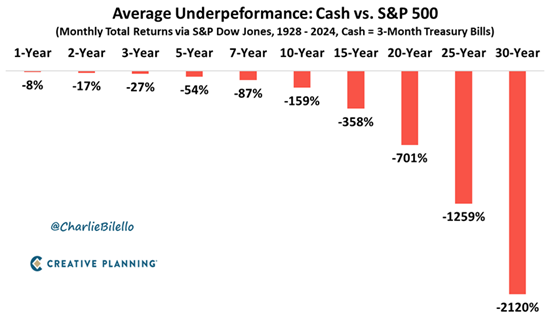

Is Cash a Good Long-Term Investment?

With short-term yields still in the 3–4% range, it’s easy to see why cash feels comfortable right now. But history reminds us that cash isn’t built for long-term growth. Over time, inflation quietly chips away at its value, even when rates are high.

Cash has its place—it provides stability and flexibility for near-term needs. Beyond that, though, holding too much can work against long-term goals. For those waiting for the “right time” to invest, putting money to work gradually on a monthly or quarterly schedule can help smooth out market swings and reduce the stress of trying to time things perfectly.

The goal is balance: keep enough cash to feel secure, but not so much that it slows your progress.

Conference Takeaways

Future Proof Conference – Huntington Beach, CA

Last month, I spent a few days at the Future Proof conference in Huntington Beach—a unique event that brings together some of the most forward-thinking voices in wealth management. Unlike the traditional conferences focused on legacy institutions, Future Proof is about what’s next: how technology, regulation, and human advice intersect in a rapidly changing world.

A major theme this year was artificial intelligence and its role in financial planning. The takeaway wasn’t that technology replaces advisors—it’s that it can help us serve families more efficiently and personally. It reaffirmed why Pomona was built the way it is: embracing innovation where it adds value, but keeping the human relationship at the center.

Alternative Investment Forum –Boulder, CO

I recently also attended the Alternative Investment Forum (put on by Harrison Street Private Wealth) in Boulder, Colorado, where I met with managers across private real estate, infrastructure, senior housing, farmland, private debt, and timberland. The private markets continue to evolve, offering new ways to diversify returns outside traditional stocks and bonds.

Events like this are part of my ongoing due diligence—continuing to learn, ask questions, and evaluate opportunities to keep Pomona’s investment approach on the leading (but not bleeding) edge.

In Closing

The first three quarters of 2025 have delivered more than most expected from the markets—but they’ve also underscored the importance of diversification across global markets, disciplined rebalancing, and thoughtful coordination between accounts. Our focus remains on navigating both opportunities and risks, while keeping your plan grounded in what matters most.

As we head into the final stretch of the year, it’s an ideal time to review portfolios, update tax estate strategies (estate documents, Donor-Advised Funds, Roth conversions, QCDs, and more), and make sure everything still aligns with your long-term goals.

If you have questions about your portfolio, financial plan, or recent headlines, feel free to reach out. You can schedule a meeting with us HERE.

Warmly,

Kevin Floyd, CFA, CFP®, AIF®

Pomona Wealth Management