Welcome to the Q1 2025 Pomona Newsletter

“We have to invest in a world we live in, and not the world we want to.”

- Charlie Munger

I had started to write this quarter’s update just after the end of March… then came the tariff threats, retaliatory announcements, partial pauses, and ongoing discussions. Volatility returned in a meaningful way, reminding us that investing isn’t just about capturing upside—it’s about having the patience and discipline to ride through uncertainty.

As always, please let me know if you have any questions or would just like to chat. My cell is (509) 643-6028 or schedule a virtual/in-person meeting HERE if that is preferable.

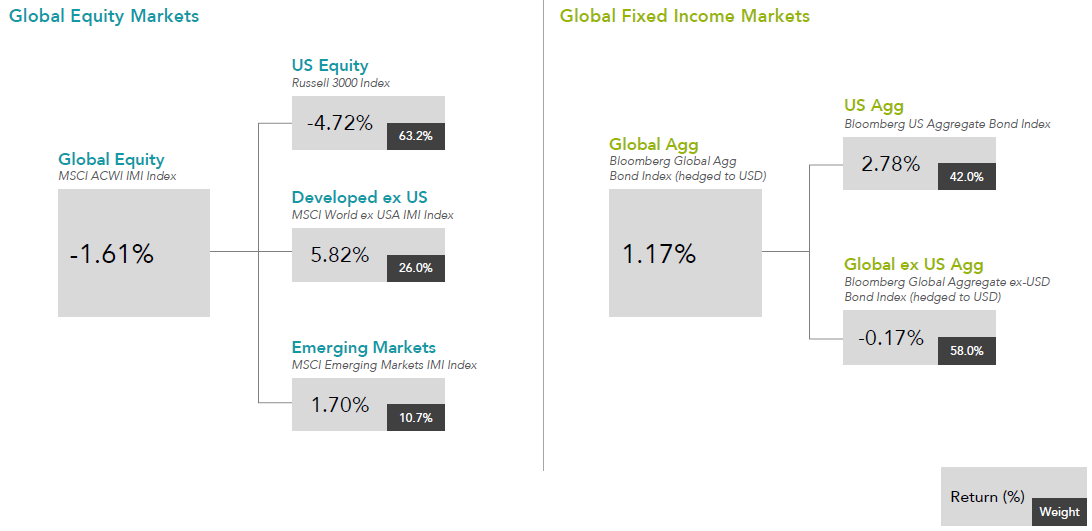

Markets Recap: Q1 2025

After a strong start to the year, markets were jolted in March. The US market ended the quarter with a decline of -4.72%, driven by a sharp selloff in major tech names. The so-called “Magnificent 7”—Apple, Microsoft, Nvidia, Alphabet, Amazon, Meta, and Tesla—saw a collective pullback of nearly 15% from February highs, dragging the index into correction territory by late March.

In contrast, international equities outperformed U.S. large-cap stocks, aided by a softer U.S. dollar and more reasonable valuations. The developed international stocks posted a +5.82% return, while emerging markets were up 1.70%. These results reinforced the importance of global diversification, especially when U.S. markets become highly concentrated in just a few names.

Bond markets also found their footing. The US bond market rose +2.78%, as yields leveled off and investors rotated into fixed income amid recession concerns. With inflation moderating and the Federal Reserve holding steady on rates, the tone in fixed income has shifted from defense to opportunity.

Economic Snapshot

The economy entered 2025 with strength, but signs of deceleration are emerging.

- Consumer spending, which makes up nearly 70% of U.S. GDP, surged in Q4 2024 by +4.2%, driven by 22 consecutive months of real wage growth and record household wealth.

- Business investment slowed, as higher borrowing costs began to take a toll, while residential investment rebounded due to easing mortgage rates and low housing supply.

- Q1 GDP, however, is on watch. A large increase in imports—likely due to companies rushing to get ahead of tariffs—could lead to a negative print due to a drag from net exports.

- Consumer confidence dropped to multi-year lows, and vehicle and retail sales both trended downward, pointing to more cautious household behavior.

While it's too early to call a recession, the economy appears to have downshifted. The question now is whether this is a temporary pause or the beginning of something more prolonged.

The Tariff Storm

Geopolitical tensions and rising protectionism have pushed trade back into the spotlight. The Trump administration’s renewed focus on tariffs—this time more heavily targeted at trade deficits—has unsettled markets and global partners alike.

While the intention is to protect American industries and address unfair trade practices, the mechanism—broad-based tariff increases—has historically been a blunt instrument. Rather than targeting specific sectors or behaviors, this approach risks fueling inflation, disrupting supply chains, and inviting retaliation.

From a broader perspective, U.S. trade deficits have long served a key role in the global economy. By exporting more dollars than we import goods, the U.S. supports dollar liquidity worldwide and maintains its position as the world’s reserve currency. Unwinding this dynamic abruptly could not only weaken that role but also reduce our influence on global policy and diplomacy.

Markets have reacted sharply to the tariff headlines, not just due to economic implications but because the policy process has lacked clarity. Greater transparency, measured steps, and Congressional engagement could ease some of this uncertainty—but none of that appears imminent.

Portfolio Updates

Equities

Our stock portfolios remain globally diversified, with a focus on high-quality and attractively valued companies. As the U.S. market has become increasingly top-heavy, we’ve continued to emphasize diversification—both by region and by style. Our non-U.S. equity exposure provided meaningful ballast this quarter, especially as the dollar declined and domestic tech valuations corrected.

This market reset also creates opportunity. Corrections allow disciplined investors to buy strong companies at more reasonable prices—something that felt impossible just months ago. We are using these moments to rebalance and reposition toward areas with better long-term return potential.

Fixed Income

Given rising risks and shifting rate expectations, we’ve taken several key steps to strengthen fixed income portfolios:

- Increased credit quality: Our allocation to AAA-rated bonds has risen from ~45% to 60%.

- Greater active management: Exposure to active strategies (primarily through Vanguard and DFA) rose from 20% to 50%, allowing for more flexible decisions around credit, duration, and sector allocation.

- More inflation protection: We doubled our allocation to Treasury Inflation Protected Securities (TIPS) from 20% to 40%, providing resilience if price pressures re-emerge.

- Maintained moderate duration: The portfolio’s average maturity remains around 6 years—long enough to generate yield, yet short enough to stay nimble

Alternatives

We continue to evaluate the role of alternative investments across client portfolios. Our view is that alternatives should serve one of two purposes:

- Reduce equity drawdown risk (e.g., managed futures / trend following, and commodities), or

- Deliver absolute returns (e.g., reinsurance, diversified alt strategies, private equity and real assets) that are uncorrelated with traditional stocks and bonds.

If alternatives are included in a portfolio, they generally make up ~10%. We may recommend adjustments based on each client’s goals and risk tolerance over the coming months. We are currently conducting ongoing due diligence across multiple strategies and may offer specific updates as warranted.

Final Thoughts: Volatility ≠ Failure

Stock market downturns are part of the journey. They don’t feel good—but they are normal. Short-term volatility, particularly when driven by politics or headlines, can cloud judgment and create emotional responses. But these are also the moments that offer long-term investors a chance to take advantage of dislocations.

As always, we remain guided by process, not predictions. We follow the financial plan, stick to disciplined portfolio construction, and rebalance thoughtfully. Whether the coming quarters bring a rebound or more bumps, we will be ready either way.

If you have questions about your portfolio, financial plan, or recent headlines, feel free to reach out. You can schedule a meeting with us HERE.

Warmly,

Kevin Floyd, CFA, CFP®, AIF®

Pomona Wealth Management