Welcome to the Spring Pomona Newsletter

“The four most dangerous words in investing are: this time it’s different.”

- Sir John Templeton

Market review: Q12026

The first quarter of 2026 reminded us why diversification still matters. U.S. stocks retreated meaningfully as the AI narrative shifted and geopolitical tension — including a Middle East conflict and an oil price spike — weighed on sentiment and pushed out expectations for Federal Reserve rate cuts. Meanwhile, international equities quietly had a strong quarter, and our alternative strategies demonstrated exactly the kind of differentiated behavior we hold them for.

What Drove the Quarter

The U.S. equity pullback reflected two forces converging at once. First, concern that AI advancement is accelerating toward disrupting established SaaS and enterprise software business models — shaking the "AI = endless growth" narrative that powered 2024–2025 returns. Second, a Middle East conflict stoked an oil price spike that the market read as inflationary, effectively pushing out expectations for near-term Federal Reserve rate cuts. The 10-year Treasury yield climbed roughly 19 basis points over the quarter, closing March at approximately 4.38%, as the market repriced for "higher for longer."

International stocks and emerging markets didn't share those headwinds to the same degree, and both posted positive quarters. After years of underperformance relative to the U.S., the beginning of 2026 is serving as a real-time case study for why we keep a meaningful allocation abroad.

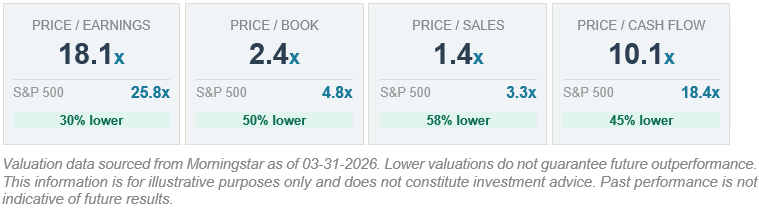

Portfolio Valuation Update

As of March 31, the equity holdings within client portfolios continue to trade at a notable discount to the S&P 500 across all four major valuation metrics. The equity sleeve is built around a mix of U.S. and international ETFs tilted toward value and high-profitability companies, which naturally results in lower price multiples than a broad market index dominated by large-cap growth stocks.

Alternatives: Doing Their job

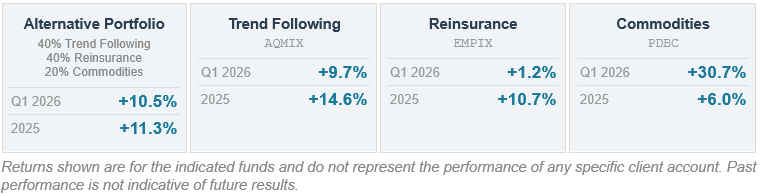

This quarter was a meaningful test for the alternative strategies in client portfolios — and they passed. While U.S. stocks (VTI) fell 4%, the alternatives composite posted a strong +10.5% for the quarter. Full-year 2025 results were equally compelling at +11.3%, demonstrating consistency, not just a one-quarter bounce.

Alternatives tend to be most impactful for clients who are at or near retirement and drawing on their portfolios. Smoothing out volatility at that stage helps manage sequence of returns risk — the danger of a sharp decline early in retirement permanently impairing a portfolio's ability to sustain distributions. For clients still in the accumulation phase with a long time horizon, a strong allocation to equities remains the most powerful wealth-building tool. Not every portfolio needs alternatives at every stage of life, but for those relying on their portfolio for income, they earn their place.

The standout was commodities (PDBC), where the oil spike associated with the Middle East conflict sent energy-linked holdings sharply higher — the same event that hurt equities was a direct tailwind here. This is a textbook example of the role commodity exposure plays: an event that creates turbulence in stocks can simultaneously act as a ballast elsewhere. Trend following (AQMIX) also had a strong showing, benefiting from clear directional moves across currencies and commodities during the quarter. Reinsurance (EMPIX) contributed modestly — its returns are driven by insurance risk and natural catastrophe events, entirely independent of equity markets or oil prices, and that's precisely the point.

A More Thoughtful Bond Portfolio

Not all bond portfolios are created equal. The typical 60/40 approach holds a broad U.S. bond index — which proved painful in 2022 when the broad U.S. bond index (AGG) fell roughly 13% as rates rose, offering no protection when clients needed it most. Our bond sleeve is built differently, with a particular emphasis on short-term TIPS (Treasury Inflation-Protected Securities) — bonds whose principal adjusts with inflation, with limited sensitivity to rising rates. In an environment where inflation and rate uncertainty remain elevated, we think that's exactly the right place to be overweight. The full lineup:

Private credit —Why We Avoided It

Private credit grew to over $2 trillion globally by 2024, with a pitch built on higher yields and seemingly low volatility. The problem was always transparency: these loans are valued internally by the funds themselves — "marked to model" rather than to market — which can mask losses until something breaks. Cracks became visible in 2024 and accelerated through 2025, with high-profile borrower collapses, gated withdrawals, and regulatory scrutiny of valuation practices.

Our job isn't only selecting what goes into your portfolio — it's equally important to recognize what should stay out. Avoiding private credit is a return that doesn't show up on a performance report, but it's real.

Tax Strategy: Bunching Gifts Into a Donor-advised Fund (DAF)

A donor-advised fund, or DAF, is a charitable giving account sponsored by a public charity — think Fidelity Charitable, Schwab Charitable, or a community foundation. You contribute cash or securities, receive an immediate tax deduction, and then recommend grants to nonprofits on your own timeline. The funds can be invested and grow tax-free in the account. It's a flexible, simplified alternative to a private foundation — with far less administrative overhead.

With the 2026 standard deduction at $32,200 for married couples filing jointly, many clients find that their annual charitable giving doesn't consistently push them above the itemizing threshold. A simple fix is "bunching" — compressing two or three years of gifts into a single year, itemizing that year, then claiming the standard deduction in off years. Your causes still receive consistent support; only the tax timing changes.

For clients in the 32% or 37% bracket the savings are even larger — roughly $5,700 to $6,600 on this same example. Donating appreciated stock to the DAF instead of cash adds another layer: no capital gains tax on the contributed shares, and the full market value is still deductible. If charitable giving is part of your plan, this is worth a conversation before year-end.

As always, please reach out with any questions about your portfolio, financial plan, or anything in the news. My cell is (509) 643-6028, or schedule a meeting.

Warmly,

Kevin Floyd, CFA,CFP®, AIF®

Pomona Wealth Management