Welcome to the Summer 2025 Pomona Newsletter

“The best time to plant a tree was 20 years ago. The second best time is now.”

-Chinese Proverb

It’s been a strong start to the first half of the year, but not without surprises. After years of U.S. dominance, international markets are finally having their moment—helped along by a quietly weakening dollar. Meanwhile, the economy continues to walk a fine line between resilience and slowdown, and markets are responding in kind.

In this quarter’s update, I’ve included a few key takeaways from the first half of 2025, as well as planning notes and thoughts on what’s driving global returns.

As always, please let me know if you have any questions or would just like to chat. My cell is (509) 643-6028 or schedule a virtual/in-person meeting HERE if that is preferable.

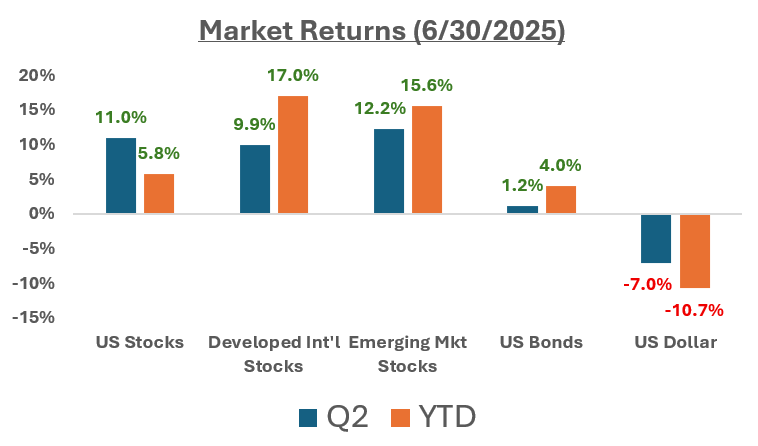

Markets Recap: Q2 2025

Through the first half of 2025, markets have delivered a strong—but uneven—set of results. The U.S. market (Russell 3000) has climbed about 11% year-to-date. After years of U.S. dominance, leadership has shifted abroad: developed international equities (MSCI EAFE) are up over 17%,while emerging markets (MSCI EM) have returned more than 15%.A key driver of this international outperformance has been the nearly 11% year-to-date decline in the U.S. dollar.

Why Global Diversification Is Paying Off

The driver behind international strength? A quietly weakening dollar. As the greenback has slipped, returns from foreign stocks have received a tailwind when translated back into U.S. dollars. This currency advantage—combined with lower starting valuations and improving global demand—has allowed international equities to gain real ground.

It’s a timely reminder: diversification still works. Holding global equities not only improves long-term performance—it also reduces the risk that any single economy, sector, or political cycle derails your portfolio. While the U.S. often leads headlines, leadership rotates over time. A globally diversified portfolio ensures you're participating wherever opportunity arises.

Policy Shifts & Planning Opportunities: What the OBBBA Means for You

This summer’s One Big Beautiful Bill Act (OBBBA) brought a wave of tax and retirement changes—many of which will shape planning decisions in the years ahead. Below are the relevant updates and what they could mean for your financial strategy.

This summer’s One Big Beautiful Bill Act (OBBBA) brought a wave of tax and retirement changes—many of which will shape planning decisions in the years ahead. Below are the relevant updates and what they could mean for your financial strategy.

Bonus Deduction for 65+ Adds Flexibility

In addition to the existing 65+ deduction, OBBBA adds a $6,000 per person bonus deduction (up to $12,000 per couple), but phased out at higher incomes. The total potential standard deduction for those over age 65 and married filing jointly is $46,700.

Why it matters: This could reduce taxable income and make partial Roth conversions more attractive—especially if we’re targeting a specific tax bracket.

Social Security: Mostly Tax-Free for Most

As mentioned above, the OBBBA introduced a new bonus deduction for those age 65+, which reduces or eliminates federal tax on Social Security benefits for about 88% of retirees. However, this benefit phases out for single filers earning over $75,000 and joint filers over $150,000 (MAGI).

Planning tip: If you're near those thresholds, strategic income planning—through RMD timing, Roth conversions, or QCDs—can help you retain the full deduction.

Farm & Business Sales: New 4-Year Deferral

If you sell qualified farmland or a closely held business, OBBBA now allows you to spread the capital gains taxes over four years instead of one.

Planning tip: If you’re considering a sale, transition, or buyout, this deferral could significantly impact your cash flow and tax strategy.

Estate Tax: Exemption Extension

The $13M+ per person estate tax exemption was scheduled to drop in 2026—but OBBBA extends it indefinitely. This reduces the urgency to gift aggressively this year, but the current exemption still offers a valuable planning window.

Bottom Line: More Tools, Not Less

OBBBA didn’t simplify the tax code, but it introduced several planning levers—deductions, deferrals, and exemptions—that can be used to reduce taxes and improve financial planning outcomes if utilized. We’ll continue to monitor developments and incorporate them into your long-term strategy.

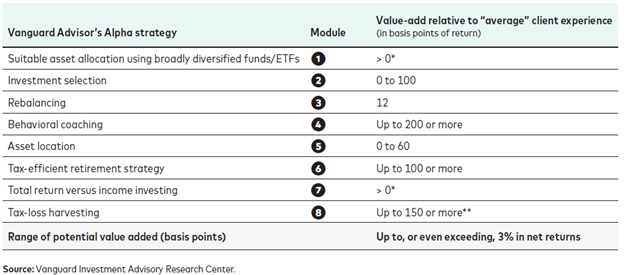

Advisor’s Alpha: Why Planning Pays Off

When markets are calm, the value of advice can be easy to underestimate. But behind the scenes, many of the most important gains come from decisions made outside of stock picking.

Vanguard’s (independent) research quantifies this as Advisor’s Alpha—an estimated 3%+ annual boost in net returns through:

- Behavioral coaching (staying the course during uncertainty)

- Tax-smart withdrawals and rebalancing

- Asset location (placing assets in the most tax-efficient accounts)

- Portfolio construction and discipline during market highs and lows

Planning Note: Rebalancing Opportunities

Every morning, we review all client portfolios to ensure they remain aligned with their target risk level. In calm markets, this often feels uneventful. But when volatility picks up, active oversight can provide a real edge.

Case in point: on April 7, following a roughly 15% market drop due to tariff concerns, were balanced portfolios that were out of tolerance—selling appreciated bonds and purchasing stocks at depressed prices. That move has since delivered an almost24% tailwind on new equity positions.

The Economy: Slowing, Stimulated, and Still Resilient

The economic data tells a mixed story. After a slight contraction in Q1 (-0.5%annualized), GDP growth is expected to remain sluggish, potentially dipping negative again in Q3—technically marking a mild recession. Still, several tailwinds are emerging:

- A reconciliation bill recently passed, triggering lower income tax withholding this year and strong refunds in 2026, which could boost consumer activity.

- Unemployment is at 4.2% (as of May) and forecasted to rise modestly to 4.5% by year-end, while wage growth holds steady at around 3.9%.

- Despite high rates, the private sector has adapted well, and consumer spending remains resilient.

Inflation has cooled, with CPI at 2.4% in May, but is projected to climb back toward 3.5%by year-end as tariffs and inventory markups ripple through prices. The Fed has held steady, with markets pricing in only one rate cut before 2026.

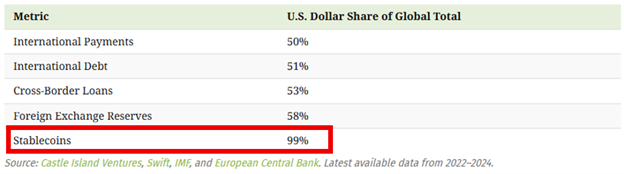

The US Dollar: Weak for Now, But Digitally Poised?

While the dollar has been under pressure recently, there are signs that longer-term strength may be quietly building—particularly as the U.S. leans into digital financial infrastructure. One key area: stablecoins.

Stablecoins are a form of cryptocurrency designed to maintain astable value—typically pegged to the U.S. dollar. Unlike Bitcoin or other volatile digital assets, stablecoins aim to offer the efficiency and speed of crypto transactions without the price swings. They’re increasingly being used for everything from cross-border payments to digital commerce and treasury management.

What’s interesting is how this evolution may actually reinforce global dollar demand. As U.S.-backed stablecoins (like USDC or PayPal USD)become more widely used, they offer a modern digital wrapper around the U.S. dollar—extending its reach in a faster, more programmable way. This could allow the dollar to maintain its global relevance even as financial systems move toward blockchain-based infrastructure.

So while the greenback has slipped this year, it may be quietly laying the foundation for a digital resurgence. We’ll be watching closely to see how this shapes both currency markets and the investment landscape in the years ahead.

In Closing

The first half of 2025 delivered more than expected in the markets—but it also revealed the growing value of diversification, discipline, and planning. We’ll continue watching for both opportunities and risks, and helping you stay grounded in what matters most.

If you have questions about your portfolio, financial plan, or recent headlines, feel free to reach out. You can schedule a meeting with us HERE.

Warmly,

Kevin Floyd, CFA, CFP®, AIF®

Pomona Wealth Management