2026 Summer Pomona Newsletter

Markets, Valuations & Washington State Planning

“Time is your friend; impulse is your enemy.”

- Jack Bogle

Market Review: The value of diversification

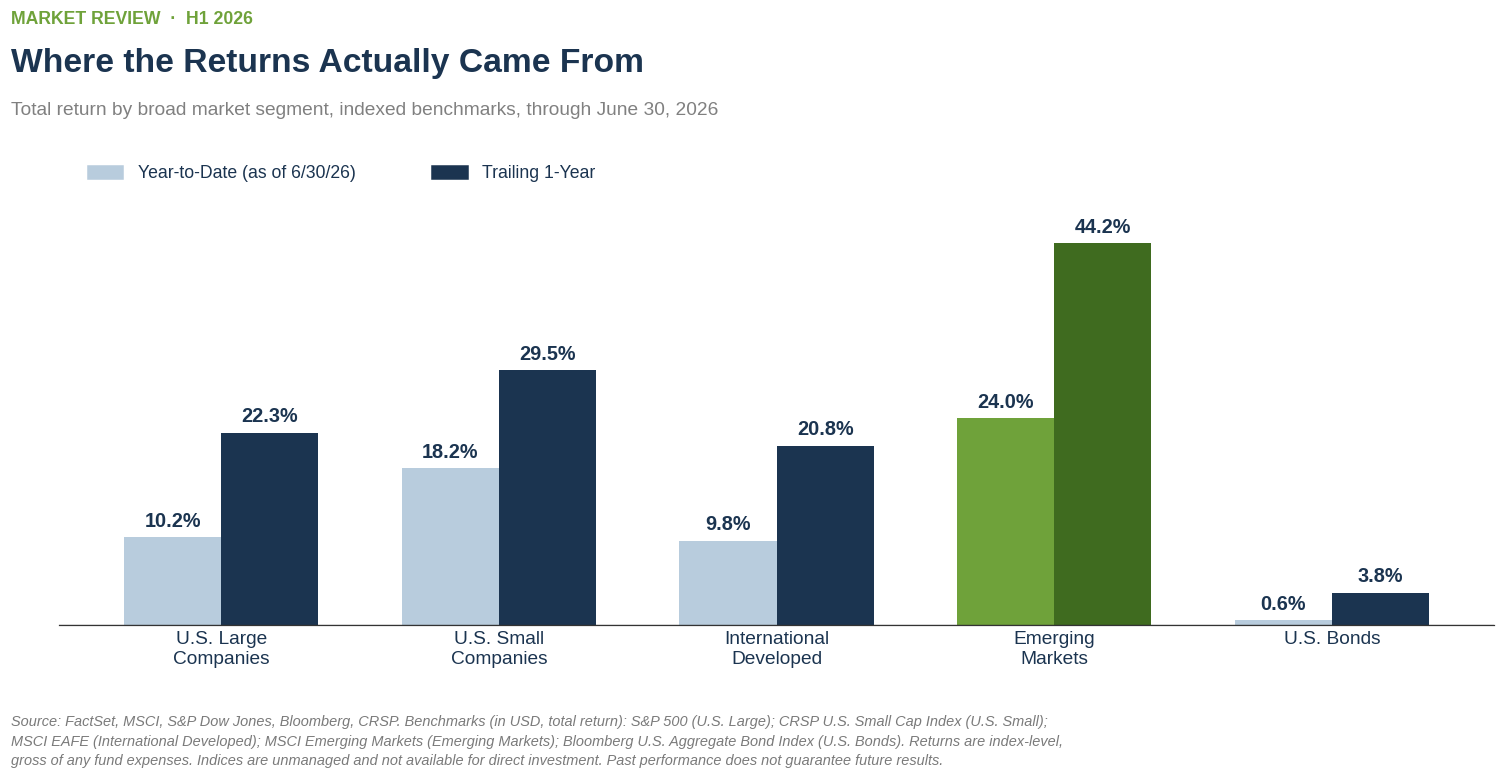

The clearest lesson of the first half of 2026 was this: staying diversified paid off. After several years in which concentrating in a handful of U.S. mega-cap technology names was the winning bet, the market's leadership broadened out substantially — and investors who held a globally diversified portfolio benefited directly.

Inflation reaccelerated during the first half of the year (headline CPI near 4.2% in May), trade policy remained uncertain, and the Federal Reserve kept its target rate unchanged at 3.5%–3.75%. Yet markets advanced anyway, as earnings growth, productivity gains tied to AI investment, and broader market participation offset those concerns.

The S&P 500 pushed to fresh highs, but the “Magnificent 7” mega-cap technology names — which accounted for an unusually large share of U.S. market gains over the past three years — were approximately flat as a group in the first half after a sharp June selloff pulled them back from earlier YTD gains. The other 493 companies in the index produced most of its H1 gain: the equal-weighted S&P 500 was up roughly 12% year-to-date, about two percentage points ahead of the cap-weighted index, and U.S. small companies and emerging-market stocks outpaced both.

To be clear, we wouldn't build our long-term philosophy around any single year. Our conviction on portfolio tilts — toward smaller, cheaper, and more profitable companies — comes from decades of data, not from six good months. Small-cap and value stocks have historically offered higher expected returns as compensation for additional risks; more profitable companies have historically outperformed less profitable ones without an equivalent step-up in risk — a quality tilt with strong academic support. Our conviction on international is different in kind: it's about diversification and more attractive relative valuations, not a claim to a persistent return premium. Any of these tilts will cost rather than pay in some years. But 2026 is a useful, live reminder of why we don't concentrate a portfolio in whatever's worked best recently — that approach looks smart right up until the year it doesn't.

Portfolio Highlight

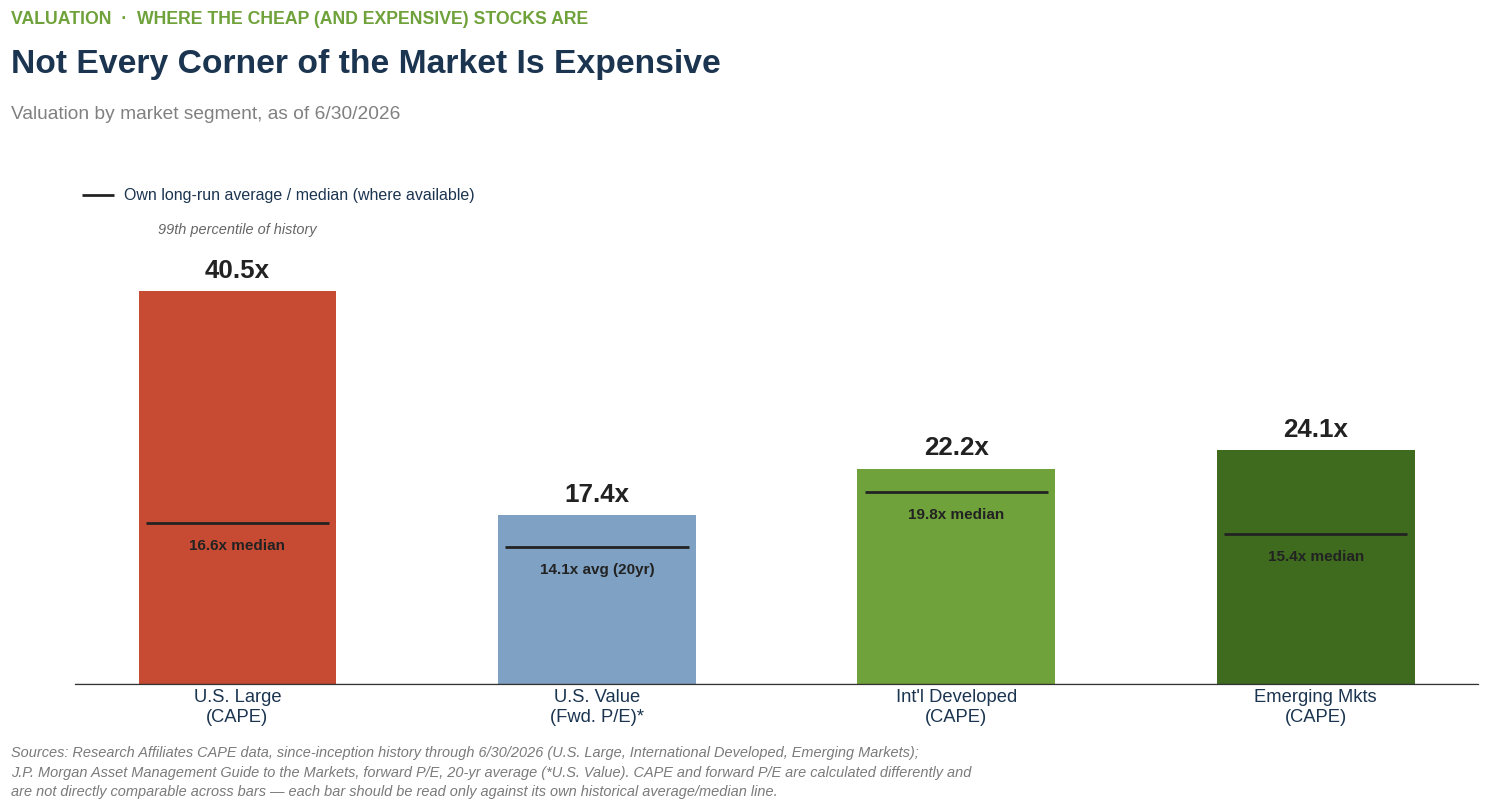

Valuations: why we remain diversified.

There's a reason we don't chase whatever won last year. Using CAPE — the cyclically-adjusted price-earnings ratio that smooths ten years of earnings to filter out any single year's noise — U.S. large-cap stocks trade at the 99th percentile of their own history back to 1880. That's a genuinely rare reading.

The point is straightforward: the U.S. large-cap market is expensive, but the rest of the market is not. U.S. value stocks are barely above their long-run average. International developed and emerging-market stocks are meaningfully cheaper than U.S. large-cap, though not deeply discounted on their own historical terms either. “The U.S. market is expensive” is really shorthand for “the largest, most tech-heavy names in the U.S. market are expensive” — there's still plenty of room to stay invested without concentrating in the most expensive corner.

None of this is a market-timing signal, and expensive markets can stay expensive for years. Currency added to that unpredictability in H1 — the dollar strengthened, which usually drags international returns, yet international still gained. The valuation gap is real, and it's one important reason we maintain a meaningful allocation to international, emerging-market, and value-oriented stocks rather than concentrating in whatever has worked best lately. For clients whose plans include them, a set of alternative strategies rounds out the portfolio by behaving differently from stocks and bonds — a further layer of diversification against any single outcome.

Planning Spotlight

Washington State: where things stand

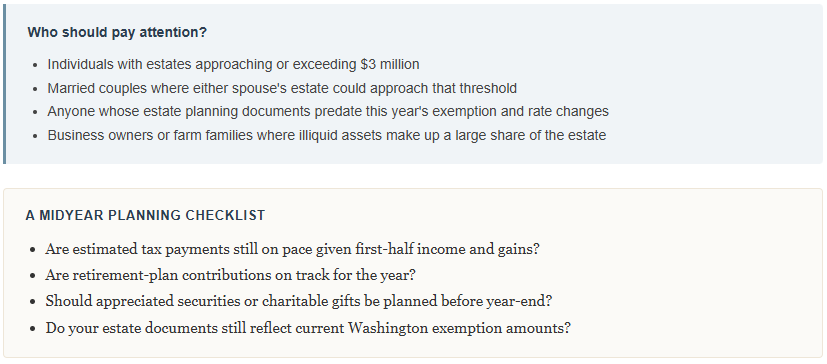

Most of our Washington-based clients are asking a version of the same question: is Washington still a good place to do business, and what's happening with all these new taxes? Here's a fair, non-partisan rundown — estate tax, business climate, and agriculture.

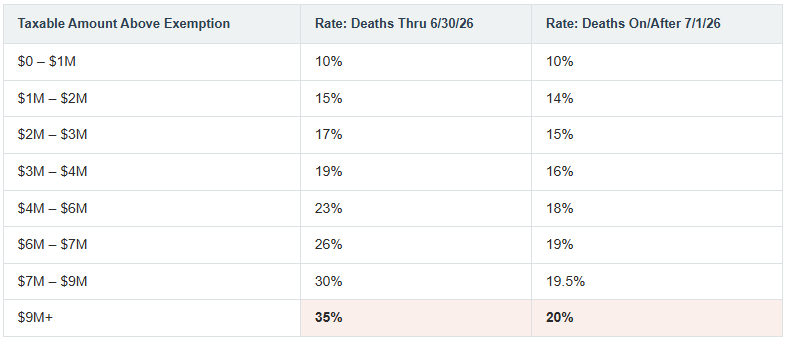

Estate Tax Is Rolling Back

After last year's increase pushed Washington's top rate to 35% — the highest in the country — Senate Bill 6347 restores a lower bracket schedule for deaths on or after July 1, 2026:

The top rate drops from 35% to 20%, and the restored rates are lower or equal in every bracket. What partially offsets that relief for estates near the threshold: the individual exclusion drops from $3.076 million (through 6/30/26) to $3.0 million (7/1/26 and after), so a slightly larger portion of the estate becomes taxable. The net effect is modest relief for estates just above the threshold and substantial relief for larger ones. Worth knowing: Washington has no portability between spouses, which means the timing and structure of an estate plan can meaningfully affect what a surviving spouse and heirs actually keep.

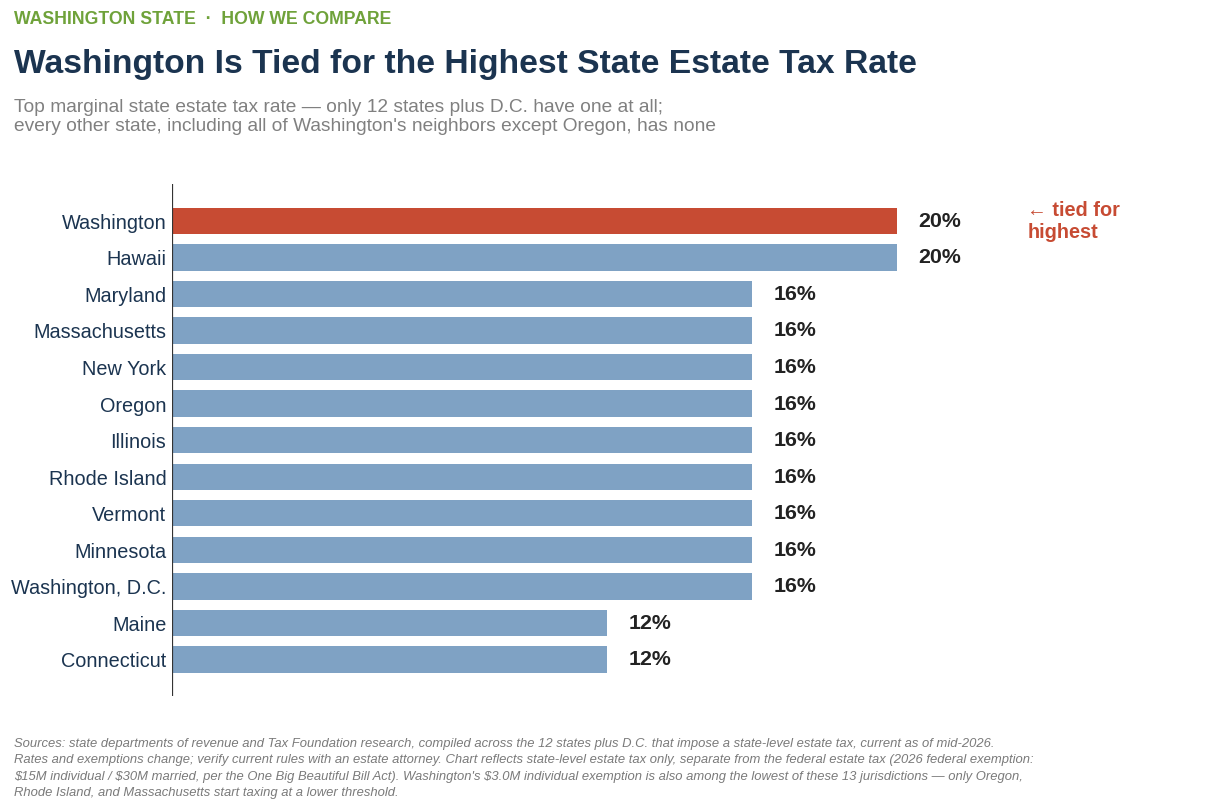

It's also worth seeing where Washington sits nationally. Only 12 states plus D.C. impose any estate tax at all:

Even after the rollback, Washington's 20% top rate is tied with Hawaii for the highest of any state, and its exemption is among the lowest of the 13 jurisdictions that tax estates. For clients with estates near these thresholds, that combination is worth a proactive planning conversation this year rather than a reactive one.

The new income tax is law, but not settled. Washington enacted its first broad personal income tax in modern history this year: 9.9% of Washington taxable income above $1 million, effective January 1, 2028, with first returns generally due in 2029. The state Supreme Court blocked a public referendum in May because of the law's emergency clause — but a separate repeal initiative has submitted more than 511,000 signatures and, if certified, would appear on the November 2026 ballot; a constitutional lawsuit is also pending. In short: it's on the books, but two live paths (the ballot and the courts) could still change that before it ever takes effect.

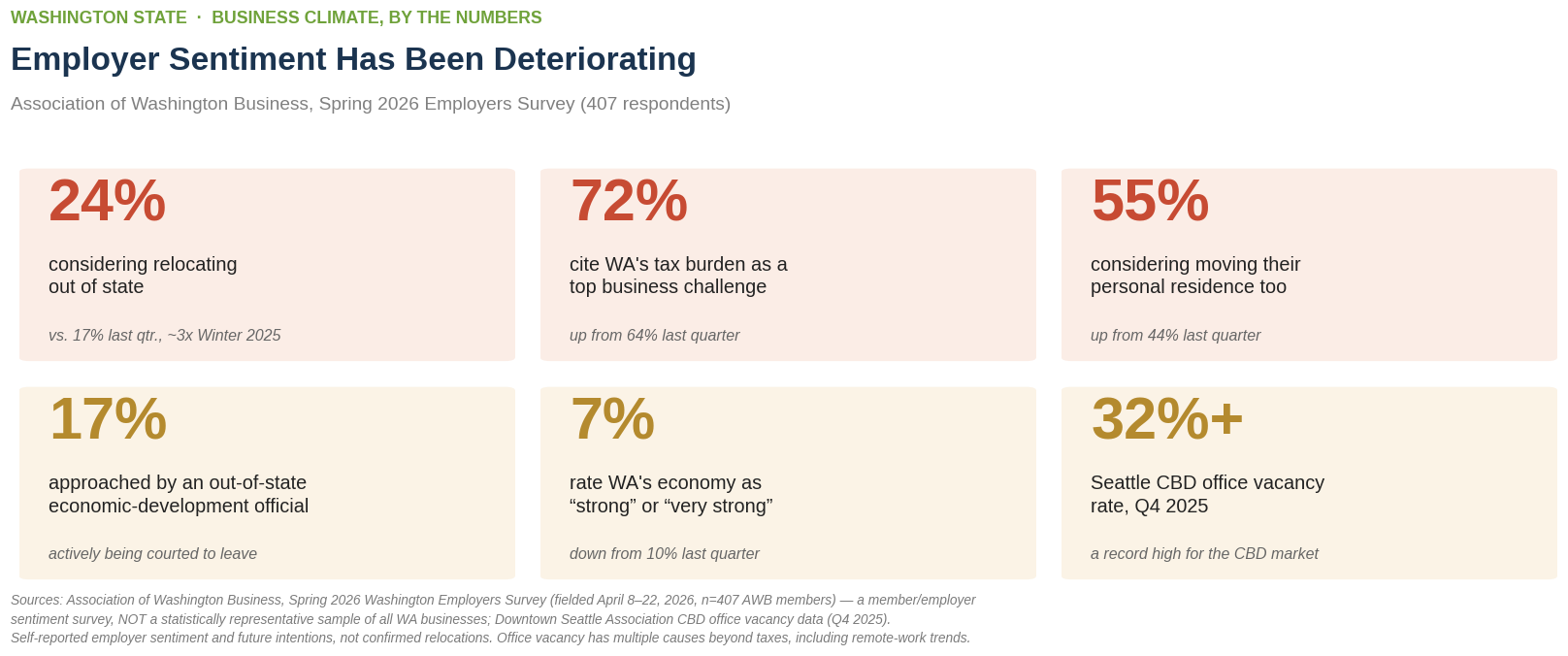

Business Climate: Mixed on Paper, More Concerning Underneath

CNBC ranked Washington #11 for business in 2026, while Chief Executive ranked Washington 47th in its 2026 CEO survey — the two use materially different methodologies. But actual employer sentiment, per the Association of Washington Business's spring 2026 survey of 407 members, points one direction:

Roughly a quarter of the 407 surveyed employers said they're considering leaving the state, and 17% reported having been approached by an out-of-state economic-development official. The AWB survey is a member/employer sentiment survey, not a statistically representative sample of all Washington businesses, and self-reported intentions aren't confirmed departures — but taken together with a record Seattle CBD office vacancy that has multiple causes beyond taxes, it's a meaningfully different signal than the rankings alone suggest. It's also not just one tax: B&O rate increases, a new surcharge, the income tax, and the estate tax changes above are all stacking at once, and the cumulative complexity is a real cost on its own, separate from the dollar amounts.

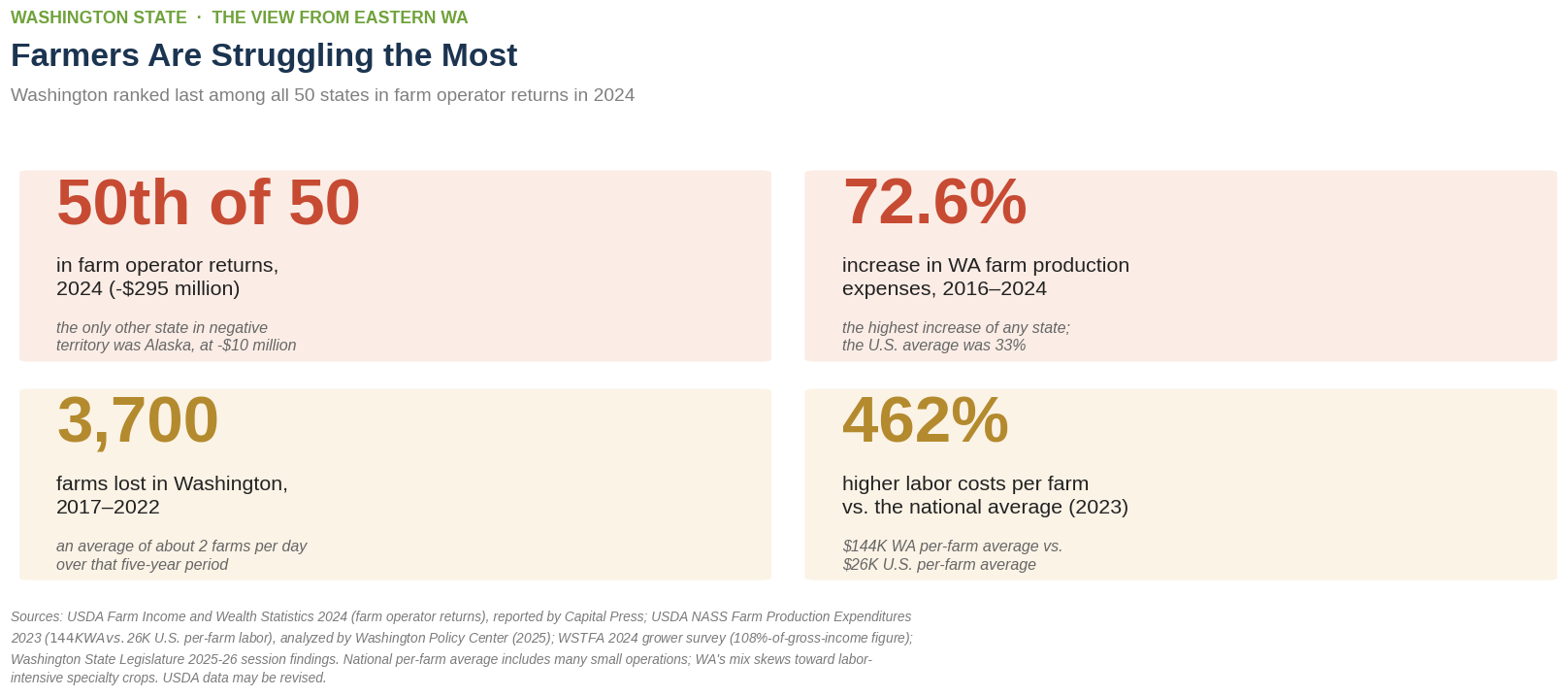

Agriculture Is Feeling a Distinct, Harder Squeeze

No state's farmers fared worse in 2024 than Washington's: dead last of any farmers in the nation — 50th of 50 states — in farm operator returns, a negative $295 million, per USDA's own data. The only other state in negative territory was Alaska (-$10 million).

Washington was also among the first states in the nation to eliminate the agricultural overtime exemption (2021 law, phased in beginning 2022), and Washington growers have faced rapidly rising labor costs since — the labor squeeze compounds the pressure on farm operator returns shown above. For clients whose operations are feeling this squeeze, it belongs in the same conversation as succession and entity planning.

These developments do not dictate a single planning response, but they increase the importance of coordinating tax, estate, business, and investment decisions for clients with businesses, farms, or estates near these thresholds.

Planning a life, not just a portfolio

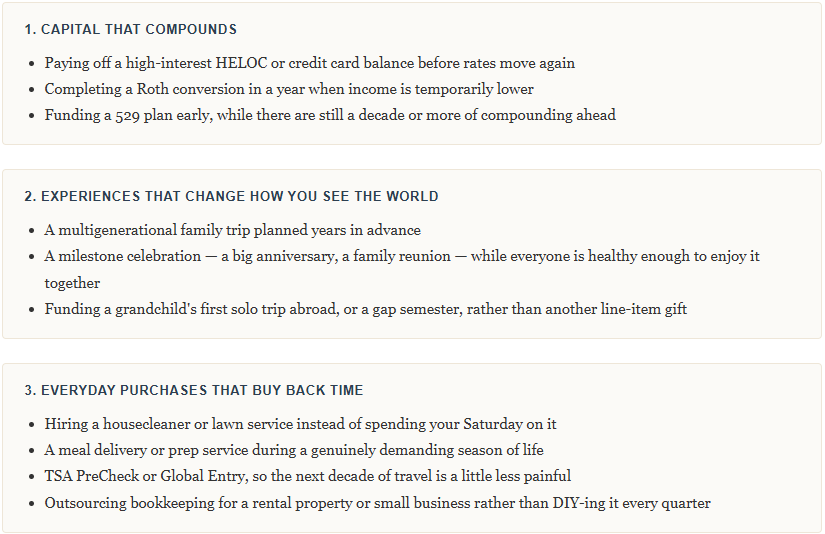

A piece that made the rounds this spring — “Spending Money for Maximum Return” — reads like a practical, everyday extension of Bill Perkins' Die With Zero, a book more than a few of you have asked us about over the years. Perkins' core argument is that most disciplined savers end up dying with far more money than they ever needed, having quietly under-spent on the experiences and moments that money was actually supposed to buy in the first place.

The core idea: money is well spent when it does one of three things — makes you more money, buys you a genuinely life-changing experience, or improves your day-to-day life in a way that pays you back in health, time, or peace of mind.

The framing we found most useful for clients thinking about retirement in particular: figure out your real “hourly number” — what an hour of your time is actually worth — and use it as a lens for every purchase decision on this list, big or small. It's a good prompt for a family conversation this summer: what would actually buy back your time, rather than just fill your house?

As always, please reach out with any questions about your portfolio, financial plan, or anything in the news. My cell is (509) 643-6028, or schedule a meeting.

Warmly,

Kevin Floyd, CFA, CFP®, AIF®

Pomona Wealth Management

Published July 2026. Market data are through June 30, 2026. Legislative, tax, and legal developments are current as of July 10, 2026 and are subject to change.

Original article: “Spending Money for Maximum Return” — The Unintuitive, May 2026. The examples above are our own, adapted for this audience rather than reproduced from the piece. If the framework resonates, Die With Zero by Bill Perkins is worth reading in full.